They interviewed 302 executives in total, representing telecom, broadcasting and media firms but only 4 percent said they were ‘very confident’ that IPTV would generate significant revenue in the coming year. Considering the longer term window, the picture of future drastically changes. In three years’ time, 34 percent of respondents ‘strongly believe’ that IPTV will generate significant revenue, while another 57 percent say that they are at least ‘somewhat confident’ that this will happen. This may be bacuse of problems faced by telcos with regard to IPTV i.e. regulation, standardisation and securing content and it is believed that they would all be resolved within three years.

The top two IPTV services that the survey group believe will offer the ‘most significant opportunities for revenue growth over the next three years’ are video on demand (19 percent of the vote) and bundled packages (15 percent). Surprises were from the advertising side that only made sixth spot (6 percent) as one of the IPTV services with most revenue potential. So tailored and interactive advertising, which IPTV can provide, is a big opportunity for wireline operators.

But the strategic worth of IPTV should not be measured in revenue growth only. As a mechanism for ‘locking in’ customers and reducing churn, IPTV will also play a valuable role. As Accenture points out in its commentary alongside the survey results, PCCW – Hong Kong’s incumbent – lost ‘tens of thousands’ of landline customers to alternate competitors three years ago. However, thanks to IPTV, PCCW has not only reduced its churn rate by 50% but expects to increase its fixed subscriber base this year. With 549,000 IPTV customers as of April 2006, PCCW has the world’s largest IPTV deployment.

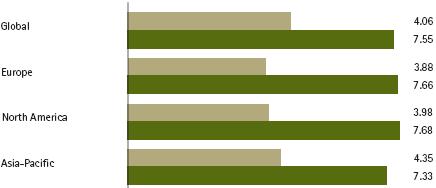

Respondents to the Accenture/EIU survey covered 40 countries in three regions: 35 percent were based in Europe; 33 percent in the Americas; and 32 percent in the Asia- Pacific. Different parts of the IPTV value chain were represented, including: equipment manufacturers (22 percent of the survey group); content providers (14 percent), integrated fixed/wireless telecoms operator (12 percent); TV broadcast network operators (10 percent); and fixed network operator/service providers (9 percent). Collating all the responses from the survey, Accenture/EIU have developed an ‘IPTV confidence index’. At the moment, confidence in IPTV as significant revenue generator in the short tern is measured at 4.06 (a ‘little confident’) on a scale of 1-10. The confidence index rises to 7.55 (‘fairly confident’) when a three-year time frame is considered.

This should come as no surprise. IPTV propels telecoms operators from the familiar territory of selling per-minute or flat-rate voice and data services into a whole new business of managing and pricing content. Breaking into IPTV creates a dilemma for operators: they must keep prices low to lure subscribers, but equally they must secure a return on their investment in infrastructure and content. This will be difficult to achieve in the short term. Survey respondents say that, over the next year, high subscription fees due to the cost of network access and/or equipment will be the greatest obstacle to IPTV adoption by households, along with quality of service issues.These barriers to market growth will diminish over time. Equipment costs will fall, and quality hitches will ease as the technology improves.

Three years from now, IPTV providers will also be bringing substantially more content to customers than today, mainly through revenue-sharing or distribution agreements with content owners, and some also through content development of their own. But content sourcing will increase costs; indeed, executives in our survey expect the high cost of content to keep subscription prices high, and that in three years this will be an important obstacle to household adoption. By then, the competitive environment will be different. Not only will telcos be vying with alternative operators for IPTV customers, but cable and DTH (direct-to-home satellite) operators can be expected to respond aggressively. Executives in the survey say emphatically that the competitiveness of offers from cable and DTH providers will be the single greatest obstacle to IPTV adoption in three years' time. Here if we can look towards telcos of developing nations we can find the solution. For example ADAE (Anil Dhirubhai Ambani Enterprises) aka Reliance is coming both in the DTH as well as IPTV space. This will help it to reduce the content cost as well as wider reach in the remote areas too. It has acquired Adlabs and Primefocus for the post production, distribution and exhibition of movies.Company is already in talks with Zee and Sony for content creation, aggregation for TV and distribution. So in long term Reliance intends to develop an entertainment strategy. This can be taken as a case study by global telcos to develop strategy for entertainment space.

With competition from cable and DTH space, operators will need to be creative, and no more so than in pricing. In the short term at least, it is their ability to bundle voice, internet and video/TV services in discounted packages that offers the greatest appeal to customers. Once the flow of content begins, most are certain that video-on-demand will be the most attractive IPTV service to customers, and the paramount revenue generator. Maybe so, but industry experience suggests they should keep their minds open.

No comments:

Post a Comment